With Wall Street heading for a 'lost decade,' Emerging Asia is expected to make a roaring comeback. | Image: shutterstock.com

Share

Portfolios with exposure to U.S. stocks and bonds could be heading for a decade of lackluster growth, according to Morgan Stanley.

Emerging Asia stocks offer a sound alternative as economies like India, South Korea, Singapore, Malaysia and Thailand have more to offer investors.

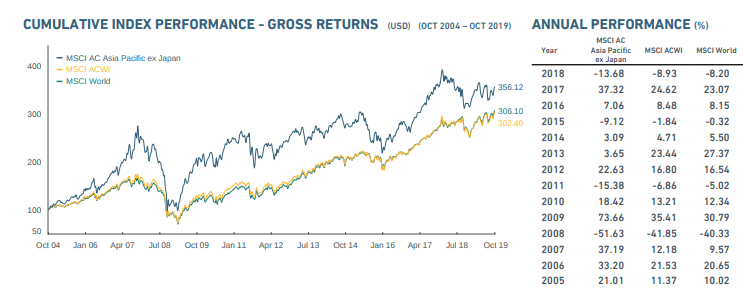

MSCI AC Asia Pacific ex Japan Index has generated gross returns of more than 356% October 2004.

Faced with diminishing growth prospects at home, investors in the United States and Europe are increasingly looking to Emerging Asia to grow their portfolios. The region has experienced miraculous growth over the past 40 years and the trend is set to continue beyond 2020 as the sun begins to set on Wall Street’s decade-long bull market.

Even if you don’t believe U.S. markets are headed for a major meltdown, it’s tough to argue that investors are buying American assets for all the wrong reasons. Last time we checked, buying assets because ‘there is no alternative’ doesn’t constitute a sound investment strategy. But that’s exactly what’s happening with U.S. stocks and bonds.

A Grim Future for Wall Street, Europe

Brexit, central-bank intervention and a never-ending ‘growth recession’ have made advanced industrialized nations less appealing for investors. Now, analysts at Morgan Stanley say these markets will offer diminishing returns over the next decade.

Over the forecast period, the analysts said a basic 60/40 split between U.S. equities and bonds will yield an average annual return of just 2.8%. That’s barely enough to stay ahead of inflation, which is targeted at 2% annually in most advanced industrialized nations.

The analysts also claim that Wall Street has a way of overestimating annual earnings – something that will come back to haunt portfolio managers in the future as profits fail to match expectations. Ironically, CCN.com covered the opposite problem last week when we reported that U.S. corporations intentionally underestimate profits and revenues each quarter to game the market.

In a nutshell: Companies and their prognosticators set the bar artificially low on earnings every chance they get. When the results are reported and earnings are ‘better than expected,’ investor sentiment is lifted and the stock rises. In the meantime, markets seem to forget that Corporate America is in the midst of its longest earnings recession in over three years.

Emerging Asia Will Lead Future Growth

While Emerging Asia has long been a major catalyst of global economic growth, the primary drivers are evolving. China, once the stalwart of emerging-market expansion, is passing the mantel (willingly or not) to countries like India, South Korea, Indonesia, Malaysia, Thailand and Singapore. Combined, these countries are reshaping the balance of power in the global economy.

China is no slouch, either. While GDP growth has slowed, China commands the world’s second largest economy and, depending on which measures you use, the largest middle-class.

Just look at these statistics: In 1980, Emerging Asia accounted for just 10% of global gross domestic product (GDP). Today, it accounts for 36% of global GDP and that figure is expected to top 50% by 2024, according to the International Monetary Fund (IMF).

In this environment, it’s easy to see why Emerging Asia is an attractive option for investors. Even if you factor decades of growth, emerging market equities are still way cheaper than their U.S. alternatives. Even Chinese stocks have a price to earnings rate that is less than half of their counterparts on Wall Street.

There’s also the fact that, among Fortune Global 500 companies, 210 are from Asia. China has a total of 129 companies represented in the group and South Korea has 16.

Although GDP growth doesn’t always translate into higher stock returns, countries in Emerging Asia should still provide better options at a time when U.S. and European markets appear overstretched, overvalued and increasingly reliant on monetary policy.

Despite recording a disappointing 2018, the MSCI AC Asia Pacific ex Japan Index has generated gross returns of 356.1% since 2004. | Chart: MSCI

The MSCI AC Asia Pacific ex Japan Index, which is a major proxy for emerging-market equities, has had a volatile few years. The index lost 13.7% in 2018 but gained 37.3% the year before. All said, the index is up in ten of the last 14 years and has returned a cumulative 356.1% since 2014.

Disclaimer: The above should not be considered trading advice from CCN.com.

Financial Editor of CCN.com, Sam Bourgi has spent the past decade focused on economics, markets, and cryptocurrencies. His work has been featured in and cited by some of the world's leading newscasts, including Barron's, CBOE, Yahoo Finance, and Forbes. Sam is based in Ontario, Canada and can be contacted at [email protected] or at LinkedIn.