A seemingly-lifeless Dow Jones Industrial Avarege (DJIA) sputtered toward the closing bell after another day of quiet trade. | Source: AP Photo/Richard Drew

Share

The Dow Jones suffered a renewed bout of paralysis on Wednesday.

With no sign of a return to normal, investors are running out of good news to power the stock market.

U.S.-China tensions are mounting, even as the coronavirus continues to fester uncomfortably throughout the country.

A seemingly-lifeless Dow Jones Industrial Average (DJIA) sputtered toward the closing bell after another day of disquietingly-rangebound trade.

With China tensions on the rise and the coronavirus showing few signs of slowing its spread in the United States, it seems Wall Street has for run out of optimistic narratives to power the Dow’s ongoing recovery.

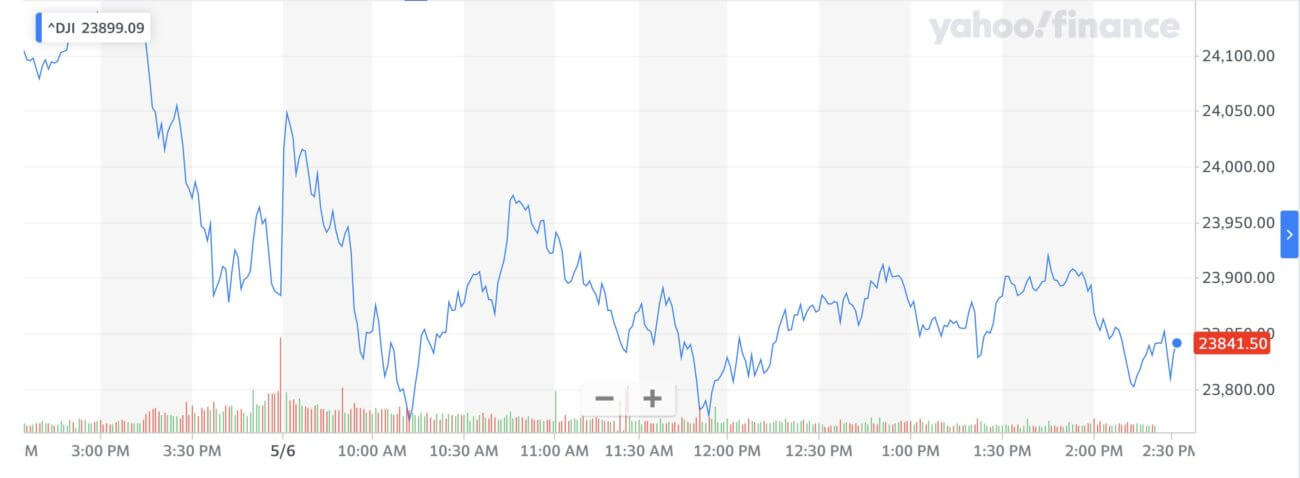

Dow Jones Slips Again as Momentum Stalls on Wall Street

The Dow Jones struggled on Wednesday as the good news ran out for Wall Street. | Source: Yahoo Finance

The Nasdaq was the only one of Wall Street’s three major indices to show signs of life. The Dow and S&P 500 traded nearly flat ahead of the closing bell:

The Dow fell 49.85 points or 0.85% to 23,833.24.

The S&P 500 dipped 0.09% to 2,865.74.

The Nasdaq rallied 0.97% to 8,894.44.

The Dow’s struggles coincided with a midweek end to oil’s relief rally. Crude dipped slightly despite the smaller-than-expected build in U.S. inventories.

WTI currently trades just under $24, which still represents a marked improvement from the devastating price movements investors saw last month.

Economic data did little to improve risk sentiment. The ADP non-farm employment reported showed a staggering 20 million job losses in the U.S.

“Absolutely No Progress In Reducing U.S. COVID-19 Infections”

It’s impossible to talk about the stock market without mentioning the outlook for the coronavirus pandemic.

And unfortunately for a United States that wants to “get back to normal,” there’s little evidence the spread of COVID-19 is truly under control.

Although many states are reopening their economies, Donald Trump has reaffirmed his commitment to keeping his pandemic task force in place, and the data does not show a nationwide plateau yet.

This has some analysts more than worried about a second assault from COVID-19. BK Asset Management Managing Director Boris Schlossberg is completely resigned to a second wave occurring.

The U.S. coronavirus infection curve shows no signs of peaking. | Source: Jim Bianco Via Twitter

He is definitely not a believer that things will get back to normal anytime soon, and he does not mince his words when discussing this seemingly-inevitable outcome:

We have of course, been highly skeptical of the “back-to-normal” trade as the underlying dynamics suggest that the return to business will be anything but normal, with many small businesses likely shuttered for good and the retail and energy sectors looking to enter Chapter 11 proceedings almost wholesale.

Add to that the fact that the US has made absolutely no progress in reducing COVID infections as the death rate moves inexorably towards the 100,000 tally while the lift of the shelter in place provisions almost guarantees the second wave of new cases.

This bearish view dovetails with the official dialogue coming out of the WHO. The health organization is nervously eyeing a disconnect between economic momentum and the number of confirmed cases.

Mike Pompeo’s new mission seems to be to attack China whenever possible, making the prospect of more tariffs extremely likely and raising the threat of a new “Cold War” between the economic superpowers.

This is a particular problem for the stock market, as Beijing appears far less restrained than usual in its retaliatory comments.

Dow Stocks: Disney Skips Dividend, Pfizer Dashes Higher

The Dow 30 was once again moving mostly sideways on Wednesday, and volatility was subdued almost across the board.

Disney (+0.55%) was marginally higher after reporting earnings. The company shelved its dividend to heighten its cash position as it tries to navigate what could be a drawn-out recovery for a company that has taken hits on multiple fronts.

Pfizer (+0.65%) rose for a second straight day as the company continues to push for a coronavirus vaccine.

Dow heavyweight Apple bounced 1.5% to carry its stock price back across the $300 threshold.

Financial speculator & author living in the hills in Los Angeles. J.D. but very much not a lawyer. Favorite trading books are anything written by Jack Schwager. | Follow Me On Twitter | Email Me