A financial analyst lays out a convincing theory that puts JP Morgan at the center of the repo market crisis. | Image: REUTERS / Aaron P. Bernstein / File Photo

Share

The repo market came front and center in September when interest rates suddenly surged.

A financial analyst reveals that JP Morgan predominantly caused the stress in the overnight lending market.

JP Morgan took liquidity out of the system to fund share buybacks and dividends.

The Fed’s intervention was supposed to be temporary. Four months later, the central bank is still hard at work to try and keep the repo market stable. On Tuesday, the Fed flooded the market with $90 billion.

There’s no sign that the Federal Reserve will stop its repo operations. | Source: Twitter

While there are numerous theories why liquidity dried up, a financial analyst reveals that JP Morgan Chase ignited the funding pressure in the repo market. I’ve been following this issue for quite some time and the latest theory looks solid.

JP Morgan Put the Fed Between a Rock and a Hard Place

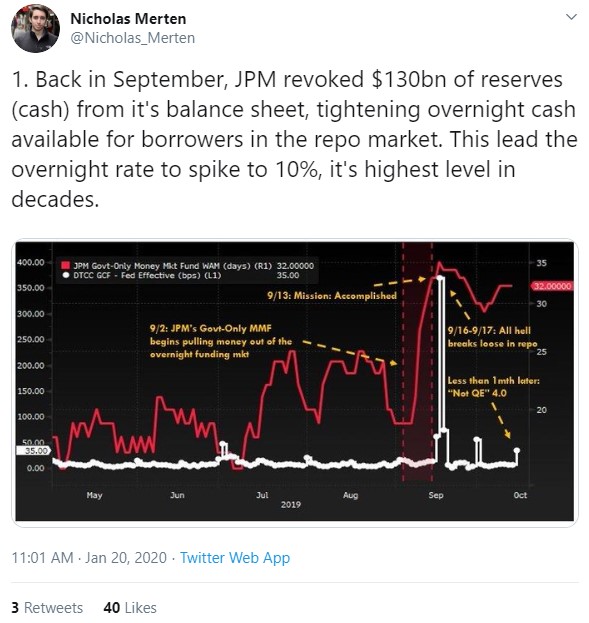

Nicholas Merten, founder of widely-followed YouTube channel DataDash, took to Twitter to explain how liquidity suddenly dried up in the short-term lending market. According to Merten, JP Morgan “predominantly caused” the repo market surge in September. The financial giant pulled out $130 billion from the overnight lending market. The sudden drop in reserves drove the overnight lending rate to soar to 10%.

JP Morgan pulling off a vanishing act. | Source: Twitter

Merten then revealed that hedge funds are the ones in dire need of liquidity, not commercial banks. He said hedge funds have opened record levels of over-leveraged positions; they need the extra liquidity or they won’t be able to cover positions with excessive leverage.

Hedge funds are in dire need of liquidity. | Source: Twitter

At this point, the Fed had a choice. They could have stay away from the repo market and watch interest rates skyrocket while stocks crash. Or they could step in, supply liquidity and keep things humming. We know how it panned out.

No way the Fed was going to let the party end. | Source: Twitter

JP Morgan Prints Big Money With the Gambit

It appears that the biggest winner of the repo market drama is JP Morgan. The investment firm suddenly had $130 billion in its pocket. That money used to make the bank 2% in the repo market. Now, they can use it to buyback shares and pump their stock.

According to Merten, JP Morgan plans to spend a whopping $32 billion on stock buybacks and dividends. That number is bigger than the bank’s net income in 2019.

JP Morgan’s $130 billion can make more money in the stock market. | Source: Twitter

JP Morgan wins twice in this situation. First, they have the liquidity to initiate a large buyback scheme. While pumping shares, they could dole out handsome dividends to attract more investors. The result is a surge in stock price.

Second, the bank forced the central bank to fund hedge funds and keep their over-leveraged positions open. As long as these hedge funds have access to liquidity, the extended bull market will likely continue. In other words, the Fed (through hedge funds) is helping drive up the price of JP Morgan (NYSE:JPM) shares.

Since September, JPM’s stock price has gone from $107.32 to 136.84, a gain of over 27%. That number is nearly twice of what the S&P 500 gained in the same time period.

Disclaimer: The above should not be considered trading advice from CCN.com. The writer does not own any JP Morgan (JPM) shares.

Kiril is a CFA Charterholder and financial professional with 6+ years of experience in financial writing, analysis, and product ownership. He has a bachelor's degree with a specialty in finance and lives in Canada.

Kiril’s current focus is on finance and cryptocurrencies.

He owns Bitcoin, Ethereum, and other cryptocurrencies. He holds investment positions in the coins but does not engage in short-term or day-trading.