A multi-disciplinary research team from the Board of Governors of the Federal Reserve System, the Federal Reserve Bank of New York, and the Federal Reserve Bank of Chicago, after conducting interviews with “approximately 30 key industry stakeholders, including market infrastructures, financial institutions, other government agencies, technology start-ups, more-established technology firms, and industry consortia,” stated in a recently published paper that, although it is unlikely, the “use of banks to conduct payments could become obsolete,” by the use of blockchain technology.

The relatively short paper [PDF], considering the nature of the study, is more an overview of blockchain technology than any insight on how it can or should be used, with the more interesting parts related to the Fed’s explanation of the current system. The paper states that payment, clearing, and settlement processes, currently, in the aggregate, process “approximately 600 million transactions per day, valued at over $12.6 trillion” in the United States alone. They do so through a hub and spoke system:

The hub and spoke system, now better known as the Lightning Network, was introduced to bitcoin’s community by Peter Todd in a highly professional video in 2013 as part of his relentless advocacy to transform bitcoin’s current payment system to one of trusted intermediaries, with its own inefficiencies and added costs the current financial system enjoys. The FED, of course, is not interested in any of that, but on what they call Distributed Ledger Technology, which they state:

“In a DLT arrangement, information regarding records of ownership and transaction histories can be distributed across the nodes in the network. Importantly, this distribution is the foundation of the technology, with the ledger of transaction histories and ownership positions shared as one common ledger that participants agree is correct.”

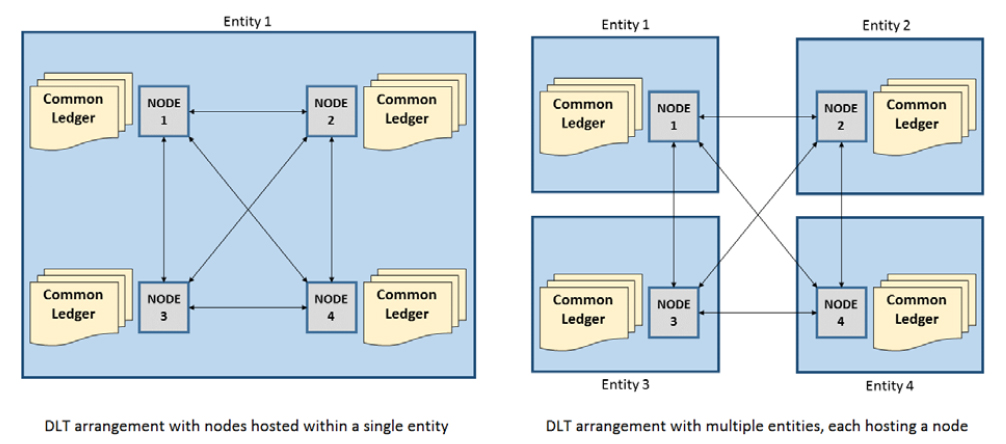

The Topology of Bitcoin and Blockchain Systems as Described by the Federal Reserve

To the left, we have an arrangement where one entity runs many copies of the same ledger. To the right, we have a representation of bitcoin, entities run their own ledger. There could be a combination of both, one entity runs many nodes and provides them as a service, while others run their own node. It is this system that is now being considered across the world for, according to the Fed’s paper, these reasons:

Reduced complexity (especially in multiparty, cross-border transactions)

Improved end-to-end processing speed and availability of assets and funds

Decreased need for reconciliation across multiple recordkeeping infrastructures

Increased transparency and immutability in transaction recordkeeping

Improved network resiliency through distributed data management

Reduced operational and financial risks

To those in the industry, the paper will probably appear somewhat bland. Lacking any guidance, or any insight, it simply provides an overview of potential benefits and risks, which indicates the FED itself is seriously considering the use of blockchain technology for its operations.

While one might have expected a thorough consideration of many aspects, with probable suggestions of how they can be addressed, the FED has provided us instead with nothing more than a graduate paper anyone could have written after an hour of googling. They tell us that blockchain technology could be used fully or in part, that it needs to interact with current structures, or does not, that there are, to the surprise of many one should think, legal considerations, questions of how one stores the keys, scalability, and the current favored, governance, considerations.

To their excuse, the paper does end by stating: “[u]nderstanding the potential range of DLT adoption and its link to changing the financial market structure is an area for future research,” but the paper does indicate the Federal Reserve is far behind, especially when one considers similar papers by the Bank of England. Nonetheless, it could not come at a better time as far as the bitcoin community is concerned. For while the Federal Reserve and the entire banking system is considering an upgrade towards a peer to peer system, the bitcoin community is currently considering a replication of the current hub and spoke financial system, with its own inefficiencies and added costs everyone is trying to address.

It is the case that, whether bitcoin is scaled on chain or forced off chain, it remains, for lack of a better word, private issued money, but how such money can compete when it moves to the inefficiencies of the current system while, at the same time, the current system moves to the efficiencies of Nakamoto’s invention, is not in any way clear. No wonder it is “very unlikely” blockchain technology could make the “use of banks to conduct payments” obsolete.