This morning The Federal Reserve Bitcoin Strategy was released in a paper outlining multiple options for improving the U.S. payment system.

In the past, Digital currency had been deemed too immature. Now, after pressure from private sector interests, the Fed is seriously analyzing the benefit of incorporating Bitcoin code in the U.S. fiat system.

“A U.S. payment system that is safe, efficient and broadly accessible is vital to the U.S. economy… the Federal Reserve plays an important role in promoting these qualities as a leader, catalyst for change and provider of payment services…”

In its preface, “Strategies for Improving the U.S. Payment System”, a white paper released Monday morning, 15/27/01, by The Federal Reserve re-affirms that commitment. The document is a follow-up to the Fed’s 2013 “Payment System Improvement – Public Consultation Paper.” At the time of the 2013 report, the digital currency was “not considered a sufficiently mature technology.” But, today, we are an “emergent payment infrastructure” and the Fed sees value for some Bitcoin technology within its current system.

“A digital transfer vehicle was not considered[sic] a sufficiently mature technology… but was identified for further exploration and monitoring gave the significant interest in the marketplace.”

In both documents, Bitcoin is never mentioned by name. Instead, the Digital Value Transfer Vehicle is used as a clever euphemism. Even though, it’s difficult to ignore the similarities to line #1 of the Federal Reserve Board’s analysis in “Bitcoin: Technical Background and Data Analysis.”

“Broadly speaking, Bitcoin is a scheme designed to facilitate the transfer of value between parties.”

Clearly, the Federal Reserve is interested in exploring what enhancements they can lift from the Bitcoin source code. Let’s take a look at their goals and see if we can’t save them some time and (our) money.

The What: (un)Desirable Outcomes

1) A ubiquitous, safe, faster electronic solution(s) for making a broad variety of business and personal payments supported by a flexible and cost-effective means for payment clearing and settlement groups to settle their positions rapidly and with finality

2) U.S. payment system security that remains very strong, with public confidence that remains high and protections and incident response that keeps pace with the rapidly evolving and expanding threat environment.

3) A greater proportion of payments originated and received electronically to reduce the average end-to-end (societal) costs of payment transactions and enable innovative payment services that deliver improved value to consumers and businesses.

4) Better choices for U.S. consumers and businesses to send and receive convenient, cost-effective, and timely cross-border payments.

5) Needed payment system improvements are collectively identified and embraced by a broad array of payment participants, with material progress in implementing them.

Aren’t outcomes one and four at odds? How do you achieve ‘better choices’ when you have ubiquitous participation? That’s like picking the presidential candidates for a two-party system and telling people “There, that’s your choice.”

Outcome two concerns violence. I will guarantee anonymity will not be a production feature in The Federal Reserve’s Bitcoin Strategy – well, not for you or me. For the simple fact that the government needs to be able to send armed men to your home to threaten, coerce or kidnap you. When the government or organizations close to the government, use the term “public confidence” they’re talking about the ability to get away with committing violence… against you.

Outcome three, they want a return on their investment. I.e. “Since you people and your bitcoins didn’t just go away we are being forced to make changes in our system. We don’t get out of bed for anything less than a few trillion. For this to be in our interest, we need to force adoption.” Plus, it plays so well with Outcome one – ubiquity.

Outcome five, “All these… individuals are implementing systems that work for them. They don’t care that it becomes a technological nightmare to get our tendrils in their books. PayPal was bad enough. Now there’s Dwolla, Stripe, Xapo, Circle, Coinbase, BitPay. This is out of control guys. You’ve had your fun but its time to come back to Papa Reserve.”

Also Read: 10 Ways Bitcoin is Better than the Federal Reserve

Color me jade, this wreaks of “We will engage the largest financial companies to discover what works best for them. Smaller organizations will be forced to change or die.”

The How: The Bitcoin Strategy

Like pioneers heading West, many of us are enticed by Bitcoin because it exists outside the current establishment. Whether for freedom or fortune, we’re here. For all our faults, not too many voices speak up in favor of making Bitcoin more like the system we’re trying to abandon.

Hey, I guess it pays to be jaded

Strategy 1: Actively Engage with Stakeholders on Initiatives Designed to Improve the U.S. Payment System

“…the Federal Reserve has substantially enhanced its level of engagement with a broad array of payment system stakeholders… will facilitate active engagement of payment stakeholders… In addition, the Federal Reserve will participate, as appropriate, in industry-led initiatives designed to further the desired outcomes.”

“We’ve got friends who put a lot of money into our careers. We can’t let the Credit Card companies or big banks down. Also, us and our friends can plan your life for you better than you can.”

Strategy 2: Identify Effective Approach(es) for Implementing Safe, Ubiquitous, Faster Payments

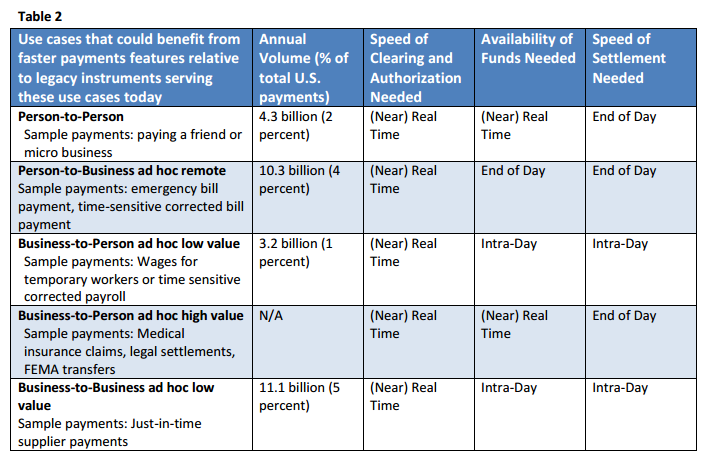

“Federal Reserve research suggests that faster speed is needed in five primary use cases encompassing at least 29 billion payments, or 12 percent of all U.S. payments annually.”

Bitcoin. Already. Does. This. Better.

It’s here, in a lonely addendum, that Digital Value Transfer Vehicles are defined:

“Digital Value Transfer Vehicles are decentralized digital stores of value that can be exchanged.”

Although it is never mentioned by name, there is one technology that fits that bill – Bitcoin. It’s doubtful that anything built by The Federal Reserve will run on Bitcoin directly. However, given the due diligence of government contractors in the past, there will likely be some copy/paste action happening.

This is part of the beauty of Bitcoin. The organizations it was built to replace cannot transition into the new paradigm Bitcoin brings without casting off the flaws that inspired Bitcoin in the first place. What I mean is, it is not enough for these organizations to simply replicate their business process on top of pseudo-bitcoin-code and a not-really-decentralized model. They must abandon the flaws fundamental to their identity – what makes them what they are.

A fractional reserve banking system has no use besides Bitcoin. It’s not that we need The Federal Reserve 2.0. It’s that The Federal Reserve is made entirely obsolete by Bitcoin.

During the industrial revolution, thousands of skilled blue-collar laborers were replaced by machines that increased production beyond imagination. Why should the digital revolution be any different? Software protocols can replace skilled white-collar workers. Bitcoin makes obsolete a closed-door finance industry that works against the consumer. Trying to assimilate some of Bitcoin’s benefits with the Fed is like scrubbing a stain with a filthy rag.

Strategy 3: Reduce Fraud Risk and Advance the Safety, Security, and Resiliency of the Payment System

Placing high priority on improving authentication of transactions, parties, and equipment in the payment process and actively pursuing ways to protect sensitive information and limit its use and availability;

Seeking to share fraud and cyber threat information and analyze data to mitigate the adverse impact of threats to payment system security; and

Increasing the focus on and priority of security, making additional resources available to strengthen it

This is flawed. Perhaps this is the fork between Bitcoin and The Federal Reserve. By design, this system requires trust and permission. Bitcoin requires no sensitive information. It requires no trusted third parties and is not restricted by electronic equipment.

Oh, why don’t they share and analyze fraud and cyber threat information now? I’m sure this is just a platitude. Since, if they had been following that last bullet point prior to now I assume the second would be enacted.

Strategy 4: Achieve Greater End-to-End Efficiency for Domestic and Cross-Border Payments

This problem exists because of systems like The Federal Reserve. Bitcoin removes the need for these legacy systems, thus the improvements The Fed proposes are not necessary.

This is the act of a dying patient injecting every needle, swallowing every pill, calling every doctor to their side to squeeze out every last second of life they have left.

Strategy 5: Enhance Federal Reserve Bank Payment, Settlement, and Risk Management Services

Why bother doing it if you aren’t going to grow your organization? There’s money being thrown around. Print some of that for yourselves, why don’t yah.

This was the only section with a definitive timeline. Basically, by 2016, The Federal Reserve wants to operate its National Settlement Service (NSS) 24/7.

I’m not a banker, and government language is intentionally obtuse. I believe the NSS is the organization that settles interbank loans – perks of the fractional reserve system. Regardless, the current system accounts for 98.6% of all settlements, already.

Fedwire Funds and National Settlement Services

“In 2013, Reserve Banks recovered 98.6 percent of the costs of their Fedwire Funds and National Settlement Services, including the related PSAF. Reserve Bank operating expenses and imputed costs for these operations totaled $97.1 million in 2013. Revenue from these services totaled $96.7 million, resulting in a net loss of $0.3 million.”

That’s Not a Strategy; It’s a Tactic.

“The difference between strategy and tactics: strategy is done above the shoulders, tactics are done below the shoulders” – Sun Tzu, Art of War

And it’s par for the course. The Federal Reserve released this document to let you know it will be spending an obscene amount of money attempting to replicate an existing, free technology. After backward engineering out the good and it will add back its own bad.

This is not leadership or a catalyst for change. This is the high school bully copying your homework and making mistakes when they re-write it in their own handwriting. Instead of losing their own grade points, the bully’s errors are taken away from the rest of the classes’ grades while the bully continues operating with impunity.

Leave the bully behind in their sandbox. It’s a big world with lots of people. It’s time to give people a chance at running their own lives. If anything, a digital dollar will make Bitcoin adoption that much easier.

Images from Shutterstock.