U.S. housing starts and building permits rebounded sharply in October, but a troubling reliance on mortgage rates reveals the true extent of housing-market weakness. | Image:: shutterstock.com

Share

Housing starts and building permits rebounded much faster than expected in October.

The gains coincide with a gradual decline in mortgage rates, which continue to dictate housing market trends.

The housing market remains extremely sensitive to mortgage rates despite them being more than 3 percentage points below the long-term average.

U.S. housing starts rebounded sharply in October, while building permits jumped to fresh 12-year highs, offering signs that the real estate market is racing back to health.

But as CNBC noted in its coverage of the monthly report, the rise in real estate activity largely coincides with a gradual decline in mortgage rates. Without this crucial ingredient, the housing recovery isn’t going anywhere.

Housing Activity Rebounds in October

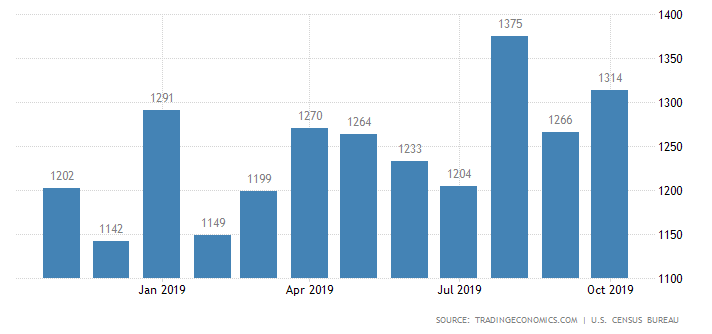

The Commerce Department reported Tuesday that housing starts jumped 3.8% in October to a seasonally adjusted 1.314 million units, far exceeding forecasts of a 0.9% increase. The September data were revised to reflect a decline of 7.9% from 9.4% reported previously.

Single-family starts in October increased 2% to a 936,000 unit pace.

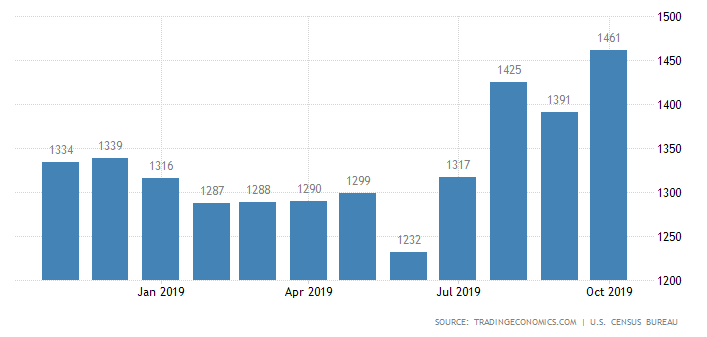

Building permits – a proxy for future construction plans – increased 5% to a seasonally adjusted 1.461 million units. That’s the highest level since May 2007. Permits for single-family housing projects increased 3.2%, reaching their highest level since August 2007.

It wasn’t just starts and permits that rose in October; housing completions shot up 10.3% from the previous month to reach 1.139 million units. That’s 12.4% higher than year-ago levels.

Another Look at the Data

On the face of it, the Commerce Department’s report offers convincing evidence that the real estate market is on solid ground. After all, groundbreaking is positively correlated with demand, so higher construction activity means more people want to buy homes.

Then you look at housing activity over the past 12 months and quickly see that starts have declined six times. That includes a brutal three-month skid through the summer where starts plunged to a seasonally adjusted 1.204 million-unit pace.

U.S. housing starts have shown extreme volatility over the past 12 months. | Chart: tradingeconomics.com

Over the same period, building permits stagnated or declined a total of six times.

Building permits rebound sharply after stagnating for much of 2019. | Chart: tradingeconomics.com

Home sales have also shown volatility, with new properties and resales declining sharply throughout the year.

Astonishingly, the National Association of Home Builders’ (NAHB) monthly sentiment index has been trending upward all year long. NAHB has been recognized as a leading lobbyist for the housing market, so take their monthly reports with a grain of salt.

The Real Factor Propping Up the Housing Market

Housing market advocates commonly cite a strengthening economy and rising wages for the increased demand in housing. They usually ignore the fact that demand hasn’t been linear in the post-crisis period, as evidenced by the volatile swings in construction activity and home sales.

One of the primary factors underpinning the housing market is mortgages. When rates rise, activity declines. When rates fall, demand increases. Although this relationship is to be expected, mortgage rates remain well below the historic average. That consumers have turned into rate watchers defies the grand narrative we are being fed about the economy.

Since the financial crisis, rising mortgage rates have adversely affected home sales. This was observed in 2014 when rates began to rise and again through 2018 when the 30-year fixed-rate mortgage peaked near 5%. Imagine a housing market buckling because average mortgage rates were 4 percentage points below the long-running average. That’s exactly what we observed last year.

Average rates have since fallen by more than one percentage point and pundits are once again touting the ‘strong housing market’ narrative. When rates rise and housing activity falls, they blame it on ‘affordability issues’ like rising house prices. Yet, rising prices are only part of the affordability crunch; the other is mortgage rates.

If the economy were so strong, the Fed wouldn’t be cutting interest rates. If consumers were so healthy, they wouldn’t be so vulnerable to a modest rise in interest rates. If the labor market were so strong, wages would be at least on par with the historic average (and certainly higher than real inflation).

Zillow Says Housing Recession Likely

Online real estate company Zillow came out with a report last month outlining the possibility of a “housing recession” in 2020. After polling 100 economists and market analysts, Zillow said the housing market is expected to hit a major snag over the next five years, with 2020 being the earliest starting point of a downturn.

The report certainly wasn’t all gloom and doom, and even offered a silver lining: A slowdown in housing may offer “welcome respite for would-be buyers” in the form of slower value appreciation.

Interestingly, the report cited concerns about rising mortgage rates overshadowing healthy demand drivers. With mortgage rates seemingly under control again, Zillow’s consensus may feel compelled to push out their forecasts for recession. But as we saw following the 2008 financial crisis, low-rate stimulus from the central bank is hardly anything to hang your hat on. The ingredients of a major downturn – not just in the housing market, but for the U.S. economy – are still ever present.

Financial Editor of CCN.com, Sam Bourgi has spent the past decade focused on economics, markets, and cryptocurrencies. His work has been featured in and cited by some of the world's leading newscasts, including Barron's, CBOE, Yahoo Finance, and Forbes. Sam is based in Ontario, Canada and can be contacted at [email protected] or at LinkedIn.