With "conventional policy" out the window, the Federal Reserve may soon embark on more radical schemes like the one being pursued by the Bank of England. | Image: REUTERS/Erin Scott/File Photo

Share

Demand for liquidity could see Fed take further unprecedented action.

Bank of England becomes first to directly finance state spending.

More central banks could follow if borrowing costs rise.

The Federal Reserve may need to provide funds directly to the U.S. government as central banks ramp up spending to tackle coronavirus.

The Fed has already pledged to purchase at least $500 billion of U.S. Treasuries as part of its unprecedented economic support package.

But it may need to go further if demand by individuals and companies for U.S. rescue schemes rises rapidly.

Fed Could Follow Bank of England

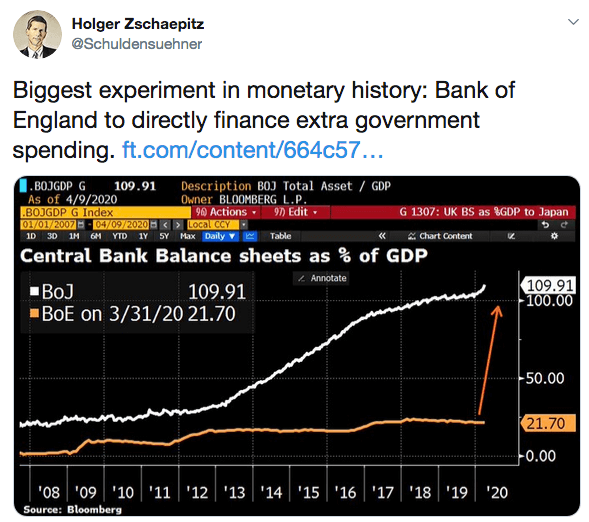

Huge demands on U.K. government coffers have seen the Bank of England become the first to directly finance state spending.

The Bank of England has become the first central bank to directly fund state spending | Source: Twitter

The Ways and Means Facility – a government bank account at the central bank – will help fund the extraordinary demand on schemes like the U.K.’s job retention program.

It stands at £400 million now but reached nearly £20 billion during the 2008-09 financial crisis. It will be needed to fund the rapidly rising number of claims for coronavirus-related government support.

The rapidly rising welfare bill might mean the U.S. needs cash more quickly than via selling bonds, the rationale for the U.K.’s move.

‘Whatever It Takes’ Means Whatever It Takes

Direct financing of the government by central banks is known as monetary financing and is hotly debated by economists.

Some find it controversial but others argue the global economy is on a war footing, making almost any financing legitimate.

Economist and Columbia University professor Joseph Stiglitz told BBC Radio 4’s Today program there had been “too much focus on the debt”.

He said:

The cost of servicing the debt in the current environment of near zero interest rates is not very significant…. When you go to war, you don’t pay attention to the debt. You say we’re going to do whatever it takes, and you do it.

Is the Fed Already There?

With open-ended rescue pledges, some believe the Fed is already engaging in something like monetary financing.

Paul Warner, senior portfolio manager at British fund manager MitonOptimal, said:

The Fed don’t need to do [monetary financing] implicitly as the dollar is the world’s reserve currency and at moment there is little likelihood that the Treasury market will be impacted by an increase in supply.

He added:

The Fed is in effect using monetary financing by buying Treasuries and mortgage-backed securities…. They say they will buy ‘at least $500bn of Treasury securities and at least $200bn of mortgage backed securities’. In other words QE infinity.”

More Direct Financing on the Way?

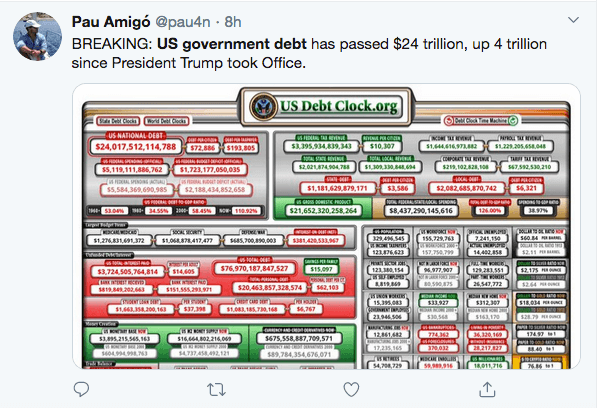

With $18 trillion of U.S. government bonds already on the market, investor demand for sovereign debt could be tested.

If supply outstrips demand, yields could rise, pushing prices down, making it more expensive for countries to borrow.

At this point, central banks could opt for direct financing.

U.S. government debt passes $24 trillion. | Source: Twitter

Australia’s Office of Financial Management (AOFM) has already raised the prospect of more competition in bond markets. This could make it harder for Australia to raise debt, especially if the world experiences a brutal L-shaped recovery.

The AOFM’s chief executive Rob Nicholl did not suggest Australia would resort to monetary financing in his March speech. But if selling debt to investors becomes harder, the Reserve Bank of Australia could take further action.

The Bank of England might not be an outlier for too much longer.

Disclaimer: The opinions expressed in this article do not necessarily reflect the views of CCN.com.

Bradley is a freelance journalist with experience in covering finance, investment, transport, and leisure for national newspapers including The Daily Telegraph and the Financial Times Group. Reach me at bgerrard63[at]gmail.com.