Faced with the biggest supply shock since the financial crisis, oil prices could be headed even lower in the near term. | Image: shutterstock.com

Share

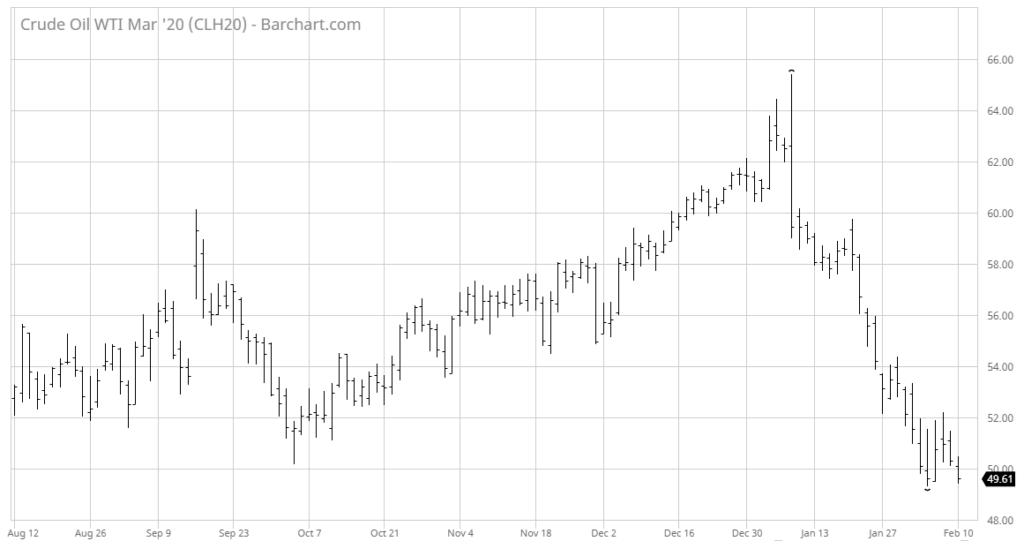

U.S. crude futures slide below $50 a barrel for the second time this month.

Chinese energy demand is said to be plunging in the wake of the coronavirus outbreak.

Russia and Saudi Arabia are at odds about production cuts, which threatens to undermine Moscow’s testy relations with OPEC.

Crude prices nosedived on Monday, as the rapidly spreading coronavirus dampened the demand outlook for oil’s biggest consumer market.

Russia and Saudi Arabia are reportedly at odds over how to adjust supplies in the wake of the negative demand shock.

Oil Prices Fall

The West Texas Intermediate (WTI) benchmark for U.S. crude prices fell nearly 2% to $49.42 a barrel on the New York Mercantile Exchange, its lowest in around 13 months. The futures contract is coming off its fifth straight weekly decline.

Oil prices have been in a severe downtrend since the second week of January. | Chart: barchart.com

Brent crude, the international futures benchmark, declined 2% to $49.42 a barrel on London’s ICE futures exchange.

Commodity prices are also being pressured by a resurgent U.S. dollar. The dollar index (DXY), a broad measure of the greenback’s performance, peaked at 98.88 on Monday, the highest since October. DXY has gained in six straight sessions.

That’s because Chinese demand for crude has plunged by around 20% in the wake of the coronavirus epidemic. It’s said that up to 400 million people across the country are under some kind of quarantine. This includes major economic centers like Shenzhen and Shanghai.

Before the outbreak, China was the world’s largest energy consumer.

The epidemic has already caused Chinese inflation to soar as businesses and supply chains faced disruption. The January consumer price index soared 5.4% annually, its highest in eight years.

Russia, OPEC Debate Production Cuts

With demand plunging, energy producers are struggling to come up with an effective response to keep prices from crashing even further.

As the de facto head of the Organization of Petroleum Exporting Countries (OPEC), Saudi Arabia wields enough power to push for compliance among its Gulf Arab neighbors. Russia, on the other hand, is an external partner that hasn’t always seen eye-to-eye on the need for deep and prolonged production cuts.

Russia and OPEC members are expected to meet later this week to discuss potential market-balancing measures. According to Bloomberg, the oil market is experiencing the biggest demand shock since the global financial crisis of 2008 to 2009.

Financial Editor of CCN.com, Sam Bourgi has spent the past decade focused on economics, markets, and cryptocurrencies. His work has been featured in and cited by some of the world's leading newscasts, including Barron's, CBOE, Yahoo Finance, and Forbes. Sam is based in Ontario, Canada and can be contacted at [email protected] or at LinkedIn.