Digital finance has great potential to improve life for consumers and merchants in India. But the lack of familiarity has impeded digital money’s growth in the country. This lack of awareness exists despite India Prime Minister Narendra Modi’s national mission for financial inclusion.

To help improve India’s digital future, the United States Agency for International Development (USAID) conducted a study identifying ways to ensure the success of Modi’s national mission for financial inclusion. The report, “Digital Finance – Beyond Cash,” examines the current behaviors and perceptions of digital payments in low-income communities in India and suggests ways to accelerate the adoption of digital payments.

The research is supported by a partnership between the India’s Ministry of Finance and USAID to increase the use of digital payments at the “point of sale,” especially among low-income consumers.

More than 35 American, Indian and international organizations joined the Ministry of Finance and USAID on this initiative. The organizations supporting the partnership include consumer goods companies, mobile network operators, payment networks, ecosystem players, e-commerce providers, and civil society organizations.

Goals: ID, Test, Scale Efforts

The goal of the research was to identify, test, and scale approaches to expand point-of-sale digital payments to improve financial inclusion.

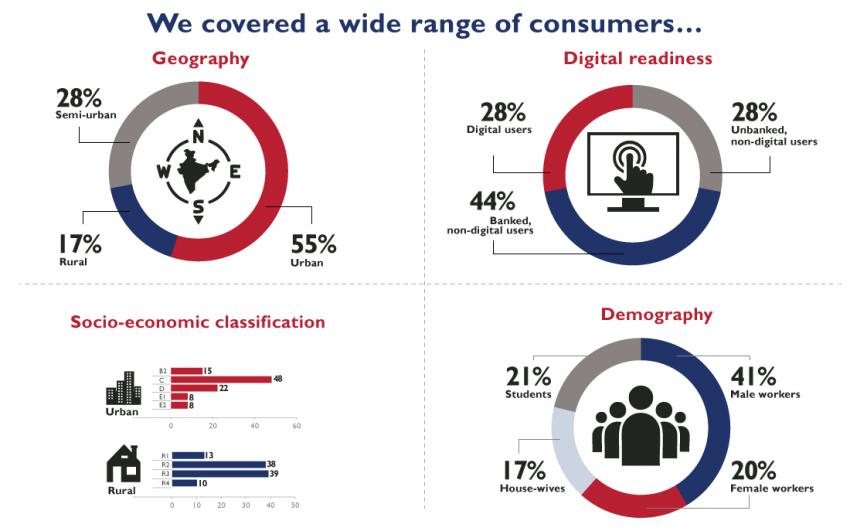

Dalberg, a global strategic advisory firm, conducted the study in six locations across four Indian states.

Digital payments have benefits for both consumers and merchants. They can spend their money more safely and securely, build credit profiles for lending opportunities that are not available in the informal banking sector, and participate in a growing online economy.

A busy road in Kolkatta

The data trail that digital transactions create can support tailored financial products such as consumer credit offerings. Digital payments can also reduce the “burden of cash” on the general economy. The Reserve Bank of India (RBI) estimated the cost of currency operations at nearly $3.5 billion annually.

Only 6% of Indian merchants currently accept digital payments. Just over 10% of Indian consumers have used a debit card for payments in the last year. These are among the findings that are somewhat surprising given the launch of the Pradhan Mantri Jan-Dhan Yojana, the government’s financial inclusion initiative.

The Pradhan Mantri Jan-Dhan Yojana has resulted in opening more than 200 million bank accounts since 2014.

The Aadhaar biometric-back identification system makes it easy for consumers to confirm their identity when opening a bank account. The Aadhaar scheme has made it possible for the -government to digitize benefit-transfers, allowing beneficiaries to keep benefit payments stored more securely.

The number of mobile phone connections has reached close to a billion in India, giving more people access to financial services. The Jan-Dhan Yojana Aadhaar Mobile (JAM) combination creates an opportunity for the country to achieve financial inclusion.

But despite this progress, the use of digital payments remains limited.

Progress Lags Despite Gains

While access to bank accounts has increased, the use of these accounts has lagged. Less than a third (29%) of bank accounts have seen use in the last three months.

The use of electronic payments like debit cards and mobile wallets is even less. While digitizing payments bring benefits, changing the everyday behavior of consumers and merchants presents a challenge in a cash-based economy such as India.

Understand Existing Preferences

Efforts to change peoples’ behavior must be based on an understanding of merchant and consumer preferences, the report noted.

The research has three goals:

• To understand the factors driving awareness among non-users of digital payments.

• To analyze the experience of current users of digital instruments such as mobile money, debit cards and online bank transfers.

• To identify strategies to stimulate adoption of digital payments among these merchants and consumers.

The research took place in the large cities of Mumbai and Hyderabad, the smaller cities of Vishakhapatnam and Kota, and in villages around Juanpur and Guntur. The research included findings from quantitative surveys of more than 2,500 respondents in addition to ethnographic research with low-income consumers and small merchants. The surveys inquired about spending and saving patterns as well as perceptions of digital payments and cash.

Key Findings in India

The first finding is that current users are highly satisfied with their digital experience. They are satisfied since they know the payment cards allow convenient access to funds. Debit card users in the lowest socioeconomic segments say the cards are safer to carry.

Mobile money users like it for its speed. They also like the discounts on airtime that come with mobile wallets, as well as the convenience. Bank transfer users like the speed and safety of these transfers.

An everyday mobile user in India

The second finding is that awareness of digital payments among non-users is low. Only 28% of those who do not hold debit cards are aware they exist and only 45% of those who are aware of debit cards want to adopt them. For mobile money and bank transfers, the interest among non-users is even lower.

Nearly all (97%) percent of retail transactions in India are made using cash or check.

Most consumers who know about digital payments have a weak digital awareness.

The third finding: Low interest in digital payments is due to the lack of a digital store of value. Consumers often do not have opportunities to convert cash to digital. They do not have opportunities to store or earn money digitally. Only 21% of those not earning money digitally save money in a bank account.

On the positive side, a strong demand exists for additional ways to save, creating an opportunity to help people build digital income. Asked if they want additional ways to save money, 55% of urban residents and 47% of semi-urban residents said they do.

The fourth finding is that the low penetration of merchant acceptance presents a barrier to digital adoption. A high percent of those surveyed were debit card users who only use cards at ATMs. This low merchant acceptance is because most consumers do not have merchants nearby who accept debit card payments.

Beyond High-Value Transactions

Digital payments most often are associated with high-value transactions, a factor that impacts wider use. Asked what payment instrument they would prefer for various-size transactions, only 4% chose a digital instrument for a transaction value of 10 rupees compared to 31% for a transaction value of 10,000 rupees.

The final finding is that consumers do recognize the problems associated with cash. Managing odd value transactions requires the merchant or consumer to have exact change. Many respondents reported having a problem with loose change. High-frequency, low-value transactions like daily transportation was a major pain point. Tracking expenditures was also cited as a major problem with cash.

The report then explored what it will take to get merchants to offer digital payments.

How To Win Merchant Support

Merchants that accept digital payments are highly satisfied. The most important benefits cited are safety, faster transactions, ease of use and less hassle involved in finding change. Mobile money acceptors cite these benefits as well as high customer appeal.

An Indian food merchant

Among merchants who don’t take digital payments, the awareness level is weak. Only 40% of those merchants who don’t take debit cards were aware they could do so. Among those who are aware, about 40% are interested in taking debit cards. These numbers are even lower for bank transfers and mobile money payments.

Following the lack of awareness, the need to use cash is the leading reason merchants are not interested in accepting debit cards. Lower consumer demand was cited as the third leading reason.

Among merchants paying suppliers in cash, 17% said they are likely to pay suppliers digitally if the supplier insists.

Ninety percent of merchants that do not pay suppliers in cash use checks.

Merchants cited the high cost of trial as a reason for not accepting digital payments.

They rank the safety of carrying cash as a major challenge, followed by managing change to return to customers. The report noted the benefit of digital payments in addressing this issue as a significant opportunity for improving merchants’ digital use.

Asked what value-added services are most attractive, merchants cited credit for business investments, less expense and easy access to working capital. This finding presents a unique opportunity for digital payments, which create a digital transaction record that can provide merchants credit.

How To Win Consumer Support

To motivate consumers to adopt digital payment, the report highlighted several opportunities.

The first such opportunity is to digitize income. Consumers who are paid digitally are more likely to conduct digital transactions. The Indian government should continue digitizing benefit transfers and consider offering incentives to organizations to pay workers digitally.

Banks can encourage employers to open bank accounts for employees and pay them digitally. Fast moving consumer goods companies (FMCGs) can encourage manufacturers to digitize worker salaries.

Banks and payment providers can develop convenient and flexible micro savings products for low-income consumers. The government should continue to introduce micro pension programs like the recently-launched Atal Pension Yojana.

An opportunity also exists to bundle savings products in government direct benefits transfers.

Digital payment solutions can address pain points of using cash for high-frequency, low-value transactions. The government should continue to digitize mass transit and other public transportation systems. It should also look at expanding transport payment instruments to broader usage.

The Octopus card, a contactless mass transit card in Hong Kong, is also used for electronic payments at stores. The RBI has allowed wallets linked to public transportation.

Banks and payment providers can develop digital products to address the challenge of managing loose change. They can create easy-to-use expense tracking with digital instruments.

The government can encourage users to extend the use of digital payments. Since existing users are well satisfied with their experience, the government can encourage digital expansion by offering monetary and tax incentives. Mobile payments and cards can link to income tax rebates.

Banks can encourage consumers to use digital payments by offering loyalty points or cash backs.

To generate interest in digital instruments, payment providers, and banks can highlight their advertising and marketing efforts on specific use cases. They can also encourage trials among new customers with incentives such as providing cash back on a customer’s first five transactions.

What To Do Next

The final section of the report highlights action ideas.

Banks and payment providers can encourage acceptance of digital payments by removing upfront fees and device installation charges. The upfront cost of trial is a big barrier to merchant acceptance. Banks can also eliminate restrictions on minimum account balances and simplify the user’s onboarding experience.

To boost retailer-to-supplier digital payments, FMCGs can encourage retailers to pay distributors digitally and offer technical assistance to them. FMCGs can provide cash backs and discounts to retailers on digital sales.

Payment providers and banks can design digital payment services that resemble characteristics of checks, such as delayed and scheduled payments.

Banks and payment providers can use transaction-based credit as an incentive for digital acceptance. They can partner with credit providers and data analytics companies to give business investment loans and working capital based on transaction data created by digital payments.

Offering credit can encourage merchants to accept digital payments. FMCGs can offer loans based on digital sales data to encourage retailers to pay distributors digitally.

Payment providers and banks can give merchants that already take digital payments incentives in exchange for bringing new merchants to digital acceptance. The government can give monetary and tax incentives to merchants for accepting digital payments.

Banks and payment providers can conduct a campaign to emphasize the benefits of digital payments, such as consumer satisfaction, safety, or lessened burden of managing loose change by communicating specific use cases.

Featured image from Shutterstock. Charts from Global Innovation Exchange.