Canopy Growth's beverage delay should worry pot stock investors. | Source: ShutterstockProfessional/Shutterstock.com

Share

Canopy Growth is revising the timeline for its cannabis beverage launch.

Management doesn’t expect the delay to impact the company’s top line in 2020.

But Canopy Growth’s bottom line is in shambles.

Canopy Growth Corp (NYSE: CGC) delayed the launch of its much-anticipated cannabis beverages. The setback is a let down for cannabis stock investors (and potheads). But the Ontario-based marijuana corporation doesn’t expect the decision to have a material impact on its revenue forecast for 2020.

Canopy’s high-profile product delay didn’t hurt the stock much today. | Source: Yahoo Finance

But pot stocks like Canopy Growth are still a long away from profitability. How long will the market tolerate their massive losses and equity dilution?

If the trend continues, it’s only a matter of time before the stock prices tank.

The Promise (and Peril) of Marijuana Beverages

The idea is promising – a marijuana-based drink that can be used medicinally or for recreation. Canopy Growth floated its new product ideas (dubbed Cannabis 2.0) at a media event in Toronto.

The company plans to offer 13 distilled, cannabis-infused beverages along with a line of cannabis-infused chocolate.

Marijuana chocolate is nothing new. But a mass-market marijuana-based drink is a potential game-changer. To get an edge over rivals, Canopy will leverage its partnership with Constellation Brands, a beverage company known for popular beers like Corona and Modelo Especial.

Canopy has had seven weeks to work with THC in the brand new beverage facility to scale processes and IP it has developed in the R&D environment. In order to deliver products that meet our customer’s high standards we are electing to revise the launch date while we work through the final details.

Canopy Growth Suffers Massive Losses and Dilution

Canopy Growth is offering unique products to the marijuana space. But eventually, investors may grow tired of the delays and abandon the stock. The company claims the delay in its cannabis beverages won’t impact on its top line for 2020.

But what about the bottom line?

Management didn’t mention the delay’s impact on Canopy’s already-massive net loss. With net losses increasing to CAD$670 million in the 2019 fiscal year (from CAD$54 million last year), the company is burning cash at an alarming rate. According to data from YCharts, negative free cash flow has already hit $1.44 billion over the trailing twelve months.

CGC has an alarming free cash flow rate. | Source: YCharts

Cash burning companies often rely on equity dilution to raise capital. Put plainly, they issue more shares. This strategy comes at the expense of investors who already own shares and can put massive downward pressure on the stock price.

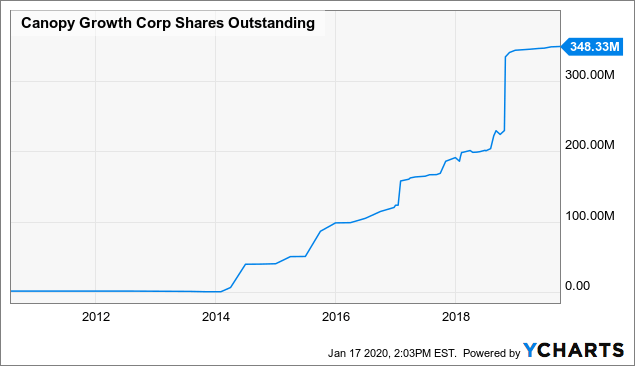

Canopy Growth has seen its number of shares outstanding balloon over the last eight years. This is due to capital raises and share-based compensation for employees. The company posted CAD$183 million in share-based compensation expenses in 2019, a staggering 517% increase from the previous year’s CAD$30 million. Revenue only grew 190% – from CAD$78 million to CAD$226 million over that period.

CGC’s number of outstanding shares has ballooned over the past eight years. | Source: YCharts

Puff, Puff, Pass!

Canopy Growth’s cannabis beverage delay is bad news. The Ontario-based marijuana company needs to scale up production as fast as possible if it wants to stay ahead of its massive losses.

While management claims the delay won’t impact 2020 revenue, there is no saying what the company’s bottom line will look like going forward.

Expect more cash burn and more dilution. Profits are nowhere in sight.

Disclaimer: The opinions in this article do not represent investment or trading advice from CCN.com

As a writer with over five years of financial experience, William Ebbs has earned millions of page views with his hard-hitting, opinionated work.

When Will isn't writing, he enjoys strategy gaming, world travel, and researching for his next article. William Ebbs is based in the United States of America. Email me | Follow Me on Twitter | Link up with me on LinkedIn