‘Rehypothecation’: More about the Wall Street Practice that Could Ruin Bitcoin

Note: This is part 4 in a multi-part article series exploring rehypothecation and commingling in bitcoin and other cryptocurrency markets. Part 1 and part 2 are interviews with Caitlin Long and parts 3 and 4 ask the question, “How did we get to a place that where laws look like this?”

The Problem with Clearing

Beyond costs to the issuers themselves, this system has resulted in a huge rise in brokerage costs with over $100 billion in post-trade servicing fees every tear. Finally, there’s the issue of ownership, something that should be hugely familiar to cryptocurrency enthusiasts who chant the mantra, “If you don’t own your private key, you don’t own your bitcoins.” This is familiar thanks to the oh-so-painful experiences of millions of bitcoin being stolen over the course of 30+ hacks . It turns out that shareholders don’t own their stocks either, with the DTCC owning 99 percent of shares. Instead what most people own and trade are “security entitlements” or the “rights and property interest of an entitlement holder with respect to a financial asset.” Shares traded today are not securities, but entitlements to underlying securities. These shares also go through a complex settlement system through the “National Securities Clearing Corporation,” yet another DTCC subsidiary. The process is outlined in the graphic below but basically consists of debiting and crediting accounts inside the DTCC. It is notable that the process is different within the new Direct Registration System (DRS), but not in a significant way for the purposes of this article.

The important thing to notice in the above diagram is that the broker, not the investor, has an account with the Depository Trust Company (DTC), a subsidiary of the DTCC. This difference is crucial because it means that the “security entitlement” owned by the investor is from the broker, not the DTC. This has some serious implications in the event of broker insolvency because action against an intermediary may be taken only in a very, very rare set of circumstances.

You might be thinking, “That’s easy if a broker goes bankrupt just take the shares and redistribute them to customers.” Well, it’s not quite that simple. The DTC holds shares in “fungible bulk,” the implication being that (as we’ve established) an individual share held with the DTC is not going to be associated with an individual shareholder. As a result of the complexity of the system we’ve spent nearly 4,000 words exploring thus far, the SEC says “imbalances can occur.” The obvious issue that arises is two-fold:

- When “imbalances” do occur, and the broker enters bankruptcy proceedings, who gets the shares?

- How does voting occur?

To take one egregious example, that’s been used repeatedly by Caitlin Long, we need to look no further than an article CCN.com wrote about Dole Foods earlier last year. Essentially, Dole had issued just under 37 million shares. The total number of shares outstanding ended up being around 49 million. There was no litigation surrounding this case, but Long made the point in a recent interview that “people lost money here” — and she’s right.

As for the voting question, firms “simply decide which of their customers will be allowed to vote.” This has resulted in one lawyer proclaiming that “in a contest closer than 55 to 45 percent, there is no verifiable answer to the question ‘who won?'” This has rendered voting on some of the closest (and most important) decisions in Wall Street history almost useless and destroyed corporate governance.

2008: Moving Beyond the Brokers

This is an issue that goes far beyond the brokers — especially today. The reason goes back to something we talked about with the introduction of multilateral netting of stocks (not other types of securities) and how it reduced counterparty risk. This was not the case for the financial instruments that caused the 2008 financial crisis. These instruments led to a large amount of counterparty risk via the introduction of collateralized debt obligations (CDOs). Ultimately, the events outlined below led to the prevalence of rehypothecation in modern markets.

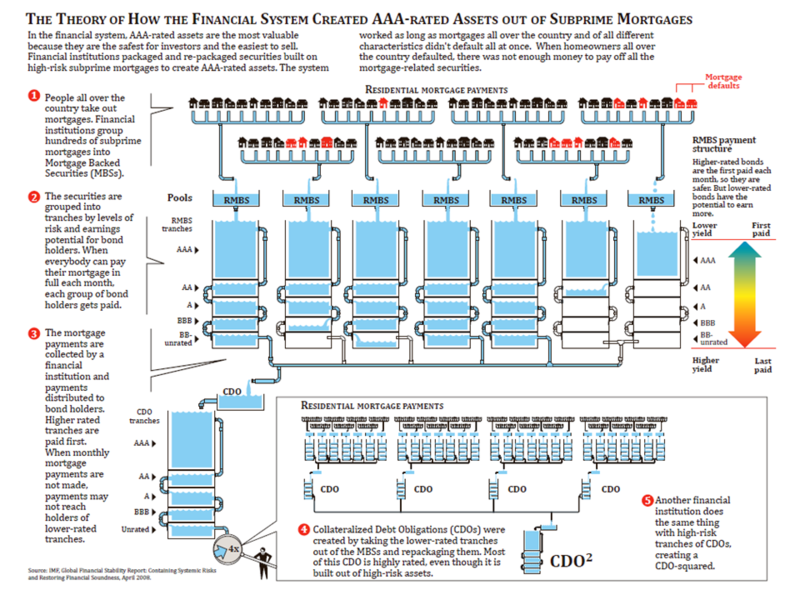

Originally, mortgage lending was very simple. A buyer would go to a bank and ask for a mortgage so they could pay off their house over the course of 15-30 years. Then, residential mortgage-backed securities (RMBS) came along and were able to dramatically increase the yield without the risk going up (at the time they were introduced mortgage default rates were 0.5 percent as opposed to well over 5 percent at the peak of the 2008 subprime mortgage crisis ).

This also allows for much higher liquidity and profits in banking. As opposed to waiting 15-30 years for a payoff, banks could now give a mortgage and sell it in no time as part of a mortgage-backed security. Even better, because of the insanely low default rates on mortgages, these bonds were AAA rated. The banks were hungry for more — and to compete and sell more mortgage-backed-securities lowered their interest rates. This wasn’t enough — there simply weren’t enough qualified people buying houses to satisfy the institutional need for RMBS.

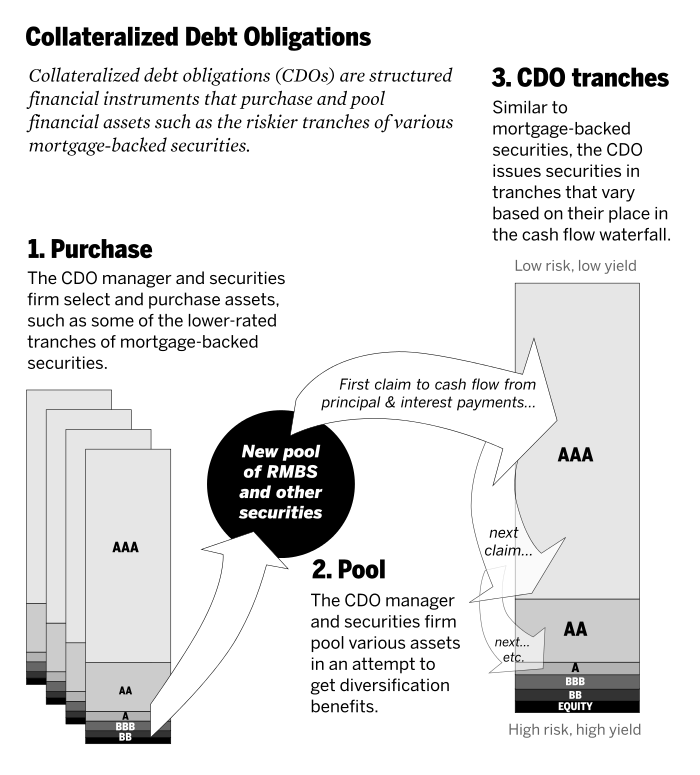

Lower-rated RBMS are then pooled together in CDOs

The bankers working on Wall Street were clever people and figured out that the way to solve this problem was to give loans to less qualified people. This started with people that had less of a cushion — but could still pay their mortgage — but ultimately ended in stories like a housekeeper owning five townhouses in Queens . The problem was that once interest rates went up, these “homeowners” couldn’t come close to covering payments on these houses and ultimately defaulted. Luckily, the financial system has a way of dealing with this by calculating risk in the form of a credit rating. If the underlying assets were bad, the RMBS should have received a bad credit rating.

The system handled this by introducing a system of “tranches” with investors being able to invest in different levels of the RMBS to receive different yields. The most “senior” level of the tranch had the lowest yield but was the safest. The lowest level of the bond had the highest yield but was most likely to fail. The bankers once again faced a problem — as subprime loaning increased and RMBS’ starting being made up of more and more lower-rated securities, the demand was not sufficient enough. Making matters worse, because of the amount that rating agencies were paid to rate these bonds (one source suggests $250,000 compared to $50,000 for municipal bonds), this meant you would have loans with mostly high-risk mortgages that were still 65 percent AAA rated.

Even with grossly inflated ratings, the banks were not happy. The lower tranches weren’t selling. Many institutional investors have rules on what credit rated bonds they are allowed to buy. Rather than taking the loss on these loans or holding them themselves the banks created what came to be known — infamously — as a collateralized debt obligation (CDO). The idea behind a CDO was that if you took enough of these lower-rated bonds — BBB, BB, and more it suddenly became “diversified.” These CDOs were still tranched, but you could repackage more subprime mortgages into AAA bonds by combining multiple lower tranche loans with some other assets resulting in 80 percent AAA ratings. Michael Lewis, the author of The Big Short: Inside the Doomsday Machine, used this analogy to explain how ridiculous this process was:

“In a CDO you gathered a 100 different mortgage bonds—usually the riskiest lower floors of the original tower … They bear a lower credit rating triple-B. … If you could somehow get them rerated as triple-A, thereby lowering their perceived risk, however dishonestly and artificially. This is what Goldman Sachs had cleverly done. It was absurd. The 100 buildings occupied the same floodplain; in the event of flood, the ground floors of all of them were equally exposed. But never mind: the rating agencies, who were paid fat fees by Goldman Sachs and other Wall Street firms for each deal they rated, pronounced 80 percent of the new tower of debt triple-A.”

Any assets that were not AAA in a bond were usually bought up by other CDOs and combined into a CDO² and ultimately ended up being rated as AAA. This process is pretty well illustrated in the diagram below.

The supply still was not enough to meet demand. In the first seven years of the 21st century, international fixed income investment hit $70 trillion compared to around $35 trillion just years earlier. There simply weren’t enough financial instruments to satisfy this need (which led to the plummeting interest rates mentioned earlier). Bankers were under pressure to sustain growth and so created what is known as a “synthetic CDO.” A synthetic CDO took advantage of a derivatives instrument known as a “credit default swap.” Essentially, it allowed third parties to bet on the outcome of specific tranched CDOs without owning the underlying assets. More significantly, it allowed them to bet by paying premiums rather than pooling money and distributing it based on the outcome. When the underlying asset went up “short” investors had to pay premiums to the “unfunded investors,” but when the CDO deteriorated (as default rates increased), the “unfunded” investors had to pay the short investors.

The issue with these “unfunded” investors is what they were really betting against was the failure of the lower-rated tranches. No one (including most of the shorts) thought that the AAA securities would fail. This resulted in higher payments to the shorts than the longs since the asset was likely not to default. More substantially, though, it meant that in the event of default there was no guarantee that the “unfunded investors” could pay. As the Financial Crisis Inquiry Commision put it:

“In the run-up to the crisis, AIG, the largest U.S. insurance company, would accumulate a one-half trillion dollar position in credit risk through the OTC market without being required to post one dollar’s worth of initial collateral or making any other provision for loss.”

AIG did not set aside reserves in the case of failure, and this resulted in a $180 billion government bailout. This cannot be blamed entirely on AIG, as AIG trusted a rating system in which the banks were essentially paying the rating agencies for good ratings. On paper, the failure of all those AAA CDOs should have been the result of a black swan event. Instead, it was just a matter of an incentive structure skewed in favor of the banks and against AIG. The sale of these shorts created a further sense of “moral hazard” with the banks. The banks, who did have visibility into the underlying assets of the CDOs they were betting against, were some of the biggest buyers of these shorts. As one expert told the New York Times, “When you buy protection against an event that you have a hand in causing, you are buying fire insurance on someone else’s house and then committing arson.”

Later on, JPMorgan was fined $296.9 million, and Goldman Sachs was fined $550 million, for their actions. The investment banks were also telling key clients (namely key hedge funds) about the composition of the CDOs, resulting in several criminal prosecutions . It’s important to note that both CDOs and Synthetic CDOs are traded bilaterally. Going back to our example above this meant that basically, every bank in the system had massive loans, liabilities, and assets in collateral with each other. This introduced an entirely new concept to the world of finance, namely, “Too Big to Fail” (TBTF). It’s important to note that the phrase TBTF does not mean banks cannot (and do not) fail. What it means is if any of these TBTF banks did fail, the contagion might bring down the entire global financial system with it. There were far more companies and individuals with exposure this time than during the paperwork crisis of 1968 (where 100 firms went bankrupt or merged), and that absolutely dwarfed the panic of 1873 (where 57 firms went under). In 2008, if the financial system failed, the world failed.

Lehman Brothers is just one example of this. Lehman, the biggest firm to go bankrupt during the crisis, ended up causing some very real damage to both retail investors and pension funds. One such investor, which ABC News reported on back in 2008, put $150,000 in a note. They were told that if the stocks performed well, they “would get a generous interest payout;” if the stock didn’t do well, “they might lose out on interest payments — but would end up holding some blue-chip shares.” This proved to be wrong, and in Hong Kong alone 43,700 people lost money in stocks that were supposed to be safe. The interesting issue here was that the issuer — Lehman Brothers — literally went out of business, and it took nearly five years to recover the shares. No one was sure that anything would be able to be recovered or how much money they would get back.

This bankruptcy, according to an Economist article written as the crisis was unfolding :

“Shredded the last remnants of confidence in American International Group, an insurer, and crystallised fears over the stability of the remaining free-standing investment banks, Goldman Sachs and Morgan Stanley. Alarm over “counterparty” risk—the risk of a borrower or trading partner failing to cough up—turned into outright terror, paralysing money markets.”

What’s interesting here is that, as you’ll remember from above, Goldman Sachs made money off the crisis. The issue was that the “unfunded” investors were defaulting left and right, and Goldman wasn’t able to collect what it was owed. This is the “counterparty” risk that directly led to the rise of today’s system. Despite the bailouts, nearly $400 billion was pulled from traditionally safe money markets and concerns over more banks defaulting led to hundreds of billions more being pulled from the markets in one of the worst recessions in history.

Reform and the Rise of the Intercontinental Exchange as a Central Counterparty Clearing House

All this background brings us to Intercontinental Exchange (ICE). It’s important to note that ICE is the company that now owns the New York Stock Exchange (in addition to several other large financial players). After the financial crash, the G20 leaders agreed to centralize credit risk. They did this through the creation of a “central counterparty clearing system” that implemented multilateral netting on all securities — OTC, foreign exchange, securities, and options. In the same way that multilateral netting reduced counterparty risk (and risk of contagion) through its introduction to the NYSE in 1892, it could also reduce counterparty risk in this system.

Multilateral netting differs in swap contracts, OTC products, and derivatives because of the introduction of “unfunded” parties and the need for collateral (rather than a mere transference of ownership for a set sum of money). Going back to the events preceding the great recession of 2008, you’ll remember that when the underlying asset went up “short” investors had to pay premiums to the “unfunded investors,” but when the underlying asset deteriorated (as default rates increased) the “unfunded” investors had to pay the short investors. You’ll also recall that because the bonds were (wrongly) AAA-rated, the firms did not put aside any kind of reserve in the case that the bond failed, leading to massive bankruptcies and companies like AIG accumulating positions in the realm of a half-trillion dollars without putting up a single cent in collateral.

To resolve these issues, central counterparties started requiring margin deposits. These deposits were not (usually) USD, and as such, could be any type of collateral. The collateral is now stored with the central counterparty, and the contract is in turn negotiated with the central counterparty. This has two effects. First of all CCP’s become “too big to fail” in a way far more severe than a bank during the 2008 financial crisis. If a CCP were to fail, it would quite literally be the end of the financial system as we know it.

Now that we understand ICE’s position on top of the financial pyramid, and how it got there, let’s explore some of the issues Caitlin Long and others have brought up when the principals on which ICE operates are brought to bitcoin.

Fractionally Reserved Banking and Rehypothecation

One of the biggest sources of counterparty risk in the modern financial system is rehypothecation. Recall that hypothecation is the pledging of shares as collateral to secure a loan (like Wall Streets firms were doing prior to the introduction of multilateral netting in 1892 to secure enough cash to meet obligations from trading). Rehypothecation, then, is the firms that shares were hypothecated to reusing the collateral they received as collateral to meet their own obligations.

Typically, rehypothecation plays out in the following manner:

- In order to increase its leverage, a hedge fund pledges $100 million worth of a security to a prime broker in exchange for a cash loan

- The hedge fund receives $95 million worth of cash (taking a 5 percent haircut) in exchange for the $100 million of securities pledged

- The prime broker now posts the $100 million worth of securities to cover its own obligations

This can go on and on increasing the size of “collateral chains.” The problem here is that if the prime broker fails, the hedge fund’s collateral can be claimed by whoever the prime broker posted their securities to. This introduces a large amount of counterparty risk into the system and is at the heart of the financial system today. The other problem is how these rehypothecated assets are accounted for. As Long writes in her post, Two Wall Street Terms Every Bitcoin Trader Needs To Learn Now , “Repo accounting under US GAAP allows each of these parties to record that they own the same asset as long as each records a different dollar of debt on its balance sheet.” The implication here is that financial institutions seem to be far more solvent than they actually are.

It’s important to note that this is only possible because of the immobilization of shares. If shares were still physically settled with individual share certificates, this would not be possible because you would own a particular share, not just one share. In the same way, every dollar bill has a unique “serial number,” and if I recorded the serial number of the dollar before I gave it to you, I could know that you gave me a different dollar bill back. If dollars were immobilized (such as in a bank account) a dollar I deposit would not be the same one I withdraw. The implication here in banking is that banks can lend out more dollars than they have (as much as 10x) without me knowing it. The same thing occurs with rehypothecation without the customers’ knowledge and is the root of much of the systemic counterparty risk in the financial system today.

The Unique Problem with Cryptocurrencies

This counterparty risk is one thing when we’re talking about traditional securities. It’s a whole other thing when we’re talking about digital assets. It turns out that there are some things unique to digitally stored assets. Putting aside the risks associated with custodianship and the allocation of profits from staking coins in a Proof-of-Stake (PoS) model. There’s another issue: hard forks.

As we’ve seen above, counterparty risk is a fact of life in rehypothecated assets. Many different parties can lay claim to the same asset. So the question becomes, “In the event of a hard fork, who actually owns the asset?”Since every party has the private keys, it could be the custodian or someone along the collateral chain.

Another issue that comes into play is voting. In the case of rehypothecated assets, who will be able to vote on hard forks? The original holder of the asset, the custodian, or someone along the collateral chain could all lay claim to that asset. As we’ve explored extensively, Wall Street has evolved a complex system of immobilized shares that are not settled in real time. The system took hundreds of years to develop and works for traditional securities (even if it isn’t optimal). Trying to apply this antiquated system to a fundamentally different type of assets simply will not work.

Featured Image from Shutterstock