Facebook Earnings: Zuckerberg Has a Dirty Little Secret

Facebook's Q2 earnings delivered significant revenue gains, but Mark Zuckerberg has a dirty little secret. | Source: AFP PHOTO / Brendan Smialowski

Despite all the issues hitting Facebook, its business continues humming along. The social media giant released second-quarter earnings and, while the stock initially jumped in after-hours trading, it has since gone flat.

The Big FB Numbers Revealed

Here are the headline numbers.

- Revenue: $16.9 billion versus $16.5 billion estimated

- Earnings Per Share (EPS): $1.99 versus $1.88 estimated

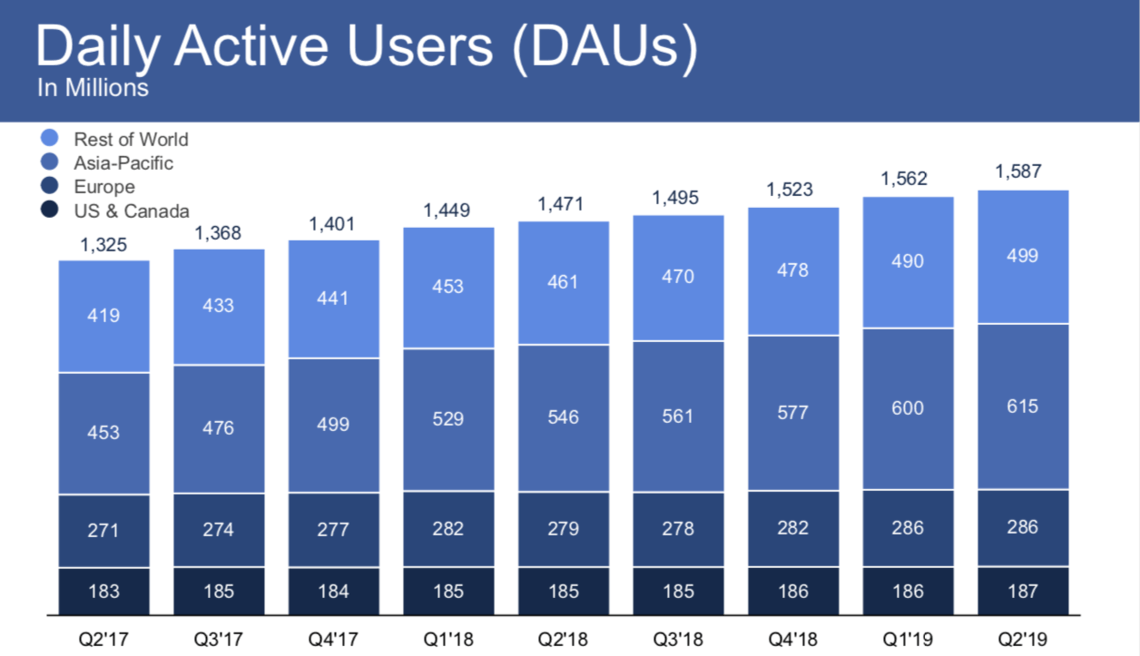

- Daily active users (DAU): 1.59 billion versus 1.57 billion estimated

- Monthly active users (MAU): 2.41 billion versus 2.42 billion estimated

Revenue not only beat estimates but grew 28 percent from $13.2 billion. Why does this matter? It tells us that advertisers not only consider Facebook to be a premier advertising platform, but they are spending more on it than last year – and by a significant amount.

A company that grows revenue 28 percent year-over-year cannot be ignored.

Facebook’s Costs Are Rising

However, costs and expenses rose by 23 percent to $9.16 billion from $7.37 billion. This does not include a multi-billion dollar charge for Facebook’s FTC settlement and another $1.1 billion on a tax-related court case that Zuckerberg and friends lost.

So while adjusted operating income grew to $7.7 billion from $5.86 billion (an increase of 32 percent), the cost to generate that increase was higher.

On the bottom line, net income excluding those significant charges came in at $5.72 billion, up only 12 percent from last year’s $5.1 billion.

The fact that advertisers continue to pony up is good news for Facebook, but with net income growth slowing to 12 percent, one wonders about Facebook’s valuation.

Facebook has about $21 billion in trailing twelve-month earnings against a net-of-cash market cap of $536 billion, meaning FB trades at 25x earnings.

However, analysts expect five-year annualized growth of 20 percent. That gives Facebook a PEG ratio of 1.25, which is not unreasonable considering its growth trajectory.

Facebook Usage Numbers Seem Fishy

Breaking down usage numbers shows another troubling picture. As the chart below shows, North American Daily Active Users have been flat for two years at 183-187 million.

Yet that number should raise suspicions. It implies that 50+ percent of the entire US population of 327 million is using Facebook every day.

Back out the 48 million under age 11, and 48 million over age 65, who likely do not use Facebook in significant numbers, and it implies that 80 percent of the population regularly uses Facebook.

That’s four out of every five people.

I’m tempted to believe that number is not completely accurate. There is simply no way that there is that level of engagement on Facebook. But even if it’s completely real, it’s bad news for Facebook, as I will explain below.

European DAUs only grew 2.6 percent to an alleged 286 million people.

US Is Dead. Only International Growth Remains

Which brings us to Mark Zuckerberg’s dirty little secret. The only real growth that occurs for Facebook is in the Asia-Pacific region, where Daily Average Users allegedly grew 15 percent to 615 million.

The rest of the world allegedly saw an 8 percent increase to 499 million people.

With the global population at 7.5 billion, and backing out China’s 1.4 billion (which does not permit the social media service), North Korea and Iran’s 120 million, the 1.5 billion kids under age 11, and Facebook’s total possible audience is not more than 4.4 billion.

We are expected to believe that half of this population uses Facebook on a monthly basis and about a third use it every day.

No way.

Facebook’s valuation is starting to get stretched, its growth is now entirely international, it faces regulatory headwinds, and the DOJ has launched an anti-trust investigation.

This explains why Facebook is launching Libra. It needs new revenue sources.

Now just doesn’t seem like a good time to buy Facebook stock.

Disclaimer: The views expressed in the article are solely those of the author and do not represent those of, nor should they be attributed to, CCN.com.